Every year, as the festive season approaches, Indian households prepare for new beginnings. For generations, purchasing gold on auspicious occasions like Dhanteras and Diwali has symbolized prosperity and good fortune. Traditionally, families would visit their trusted jeweler to buy a coin, a small bar, or an ornament, believing it would bring wealth and blessings for the year ahead.

However, gold has evolved beyond tradition—it’s now a crucial investment choice offering stability in fluctuating markets. While previous generations relied solely on jewelry or coins, today’s investors prefer Gold ETFs, Sovereign Gold Bonds, digital gold, and gold mutual funds.

In 2025, gold has delivered exceptional returns, with domestic prices rising 66% year-to-date, amplified by Indian rupee weakness. With current prices at ₹12,982 per gram for 24-karat gold and ₹11,900 per gram for 22-karat gold, understanding the best investment options is more important than ever.

This comprehensive guide will walk you through the smartest ways to invest in gold this festive season, helping you decide which option suits your financial goals—whether you’re buying for tradition, investment, or both.

Why Should Gold Be Part of Your Investment Portfolio in 2025?

In today’s unpredictable economic climate, where stock markets experience wild swings and inflation remains elevated, gold stands out as a safe and reliable investment. Beyond capital protection, it provides stability during global financial uncertainties, making it a trusted choice for investors worldwide.

Record-Breaking Performance in 2025

Gold has been the top performer in 2025, with prices reaching an all-time high of ₹384,197 per ounce on October 20, 2025. This represents a remarkable 67.88% increase from the year’s start.

Strong Market Fundamentals

Experts suggest gold prices could continue rising as central banks worldwide keep adding gold to their reserves. India’s central bank increased gold reserves to 880.2 tonnes, with the share of gold in foreign exchange reserves rising from 9% to 14% this year.

Unprecedented Investor Interest

Indian gold ETFs witnessed their largest-ever monthly net inflows in September 2025, totaling ₹83.6 billion, representing a 282% increase month-over-month. This surge reflects growing confidence in gold as a strategic investment asset.

Accessibility and Convenience

In India, investing in gold has become easier than ever, thanks to modern options like digital gold and Sovereign Gold Bonds. These allow both beginners and seasoned investors to enter the market conveniently, without worrying about storage or security concerns.

With its high liquidity, long-term value retention, and proven track record as a hedge against inflation and market volatility, gold is more than just a safe haven—it’s a strategic asset that can bring balance and security to your investment portfolio.

Key Things to Keep in Mind Before Investing in Gold

1. Know Exactly What You’re Buying

If you’re saving for a wedding or planning to purchase a specific item—say, a 10-gram gold necklace—make sure the savings agreement clearly mentions the design, weight, and total price. Having these details in writing protects you from sudden price hikes or last-minute surprises when you finally redeem your gold.

2. Check Credibility and Trustworthiness

Always research the jeweler or platform you’re dealing with. Go through customer reviews, ratings, and social media feedback. If you find repeated complaints about delayed delivery, poor product quality, or lack of transparency, it’s best to walk away. A reliable jeweler or platform will always provide clear, upfront information about their products and services.

3. Stay Updated with Market Prices

Gold prices are subject to volatility, as upticks in demand significantly impact prices due to fixed supply versus flexible demand. Prices fluctuate daily, and even small changes can make a big difference in your investment.

Keep track of prices using financial news portals or apps. If you notice an upward trend, consider buying sooner rather than later to lock in a better rate. Domestic gold prices have been trading at a premium of up to $25 per ounce as of mid-October, marking the highest level since July 2024.

4. Watch Out for Hidden Charges

Before signing any agreement or plan, carefully read the terms and conditions. Some schemes may include hidden fees, making charges (typically 8-25% of gold value), or GST (currently 3% on gold purchases) that can eat into your returns. Cross-check all details so you don’t get caught off guard later.

5. Consider Systematic Investment

Rather than lump-sum investments, experts recommend staggered or systematic monthly purchases to reconcile positive buyer sentiment with financial discipline. This approach helps you benefit from price fluctuations over time while maintaining steady asset allocation.

Popular Gold Investment Options in India

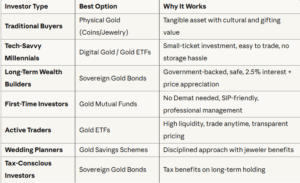

1. Sovereign Gold Bonds (SGBs)

Best for: Long-term investors seeking government-backed security

Sovereign Gold Bonds are one of the most trusted and secure ways to invest in gold since they’re issued by the Government of India. However, they’re not available year-round. Instead, the government opens subscription windows a few times a year, usually for about a week.

Key Benefits:

- Government-backed security

- 2.5% annual interest payment

- No storage concerns

- Capital gains tax exemption if held till maturity (8 years)

- Can be traded on stock exchanges

Current Status: For 2025, investors are still waiting for the government to announce the next tranche. If you miss the subscription window, you can buy previously issued SGBs through the secondary market.

Ideal Investment: ₹1 gram minimum, with no maximum limit (except for individuals at 4 kg per fiscal year)

2. Digital Gold

Best for: Tech-savvy millennials and beginners

For those who prefer convenience, digital gold is a modern alternative. Through popular apps like Paytm, PhonePe, and Google Pay, you can start buying gold with as little as ₹1.

Key Benefits:

- Ultra-low minimum investment (₹1 onwards)

- 24/7 purchase availability

- Secure storage by trusted partners (SafeGold, MMTC-PAMP)

- Can be converted to physical gold

- No making charges

- Instant liquidity

Considerations:

- Storage charges (typically 0.3-0.5% annually after first year)

- Buy-sell spread (difference between buying and selling price)

- GST applicable (3%)

Popular Platforms: Paytm, PhonePe, Google Pay, Amazon Pay, MMTC-PAMP, SafeGold

3. Gold Exchange-Traded Funds (ETFs)

Best for: Investors with Demat accounts seeking liquidity

A Gold ETF is essentially a mutual fund that invests in 99.5% pure gold. These ETFs trade on the stock exchange, just like company shares, meaning you can buy or sell units anytime during market hours.

Key Benefits:

- High liquidity—trade anytime during market hours

- No storage worries

- Lower expense ratio (typically 0.5-1%)

- Transparency in pricing

- No making charges

- Regulated by SEBI

Requirements:

- Demat account mandatory

- Minimum investment typically 1 unit (equivalent to 1 gram of gold)

Popular Gold ETFs: SBI Gold ETF, HDFC Gold ETF, ICICI Prudential Gold ETF, Nippon India Gold ETF

2025 Performance: Total gold holdings in Indian ETFs rose to 68 tonnes, with assets under management reaching ₹676 billion, representing a 96% year-over-year increase.

4. Gold Mutual Funds

Best for: First-time investors without Demat accounts

Gold mutual funds invest primarily in Gold ETFs, offering an indirect way to invest in gold without needing a Demat account.

Key Benefits:

- No Demat account required

- SIP facility available (systematic investment plans)

- Professional fund management

- Starting from ₹500-₹1,000

- Easy redemption process

- Suitable for long-term wealth creation

Tax Treatment:

- Short-term gains (less than 3 years): Taxed as per income tax slab

- Long-term gains (more than 3 years): 20% with indexation benefit

5. Physical Gold (Coins and Bars)

Best for: Traditional investors wanting tangible assets

If you want something tangible but still easy to store, gold coins and bars are excellent options. They’re available through jewelers, banks, NBFCs, and even e-commerce platforms.

Key Benefits:

- Tangible asset you can hold

- Excellent for gifting

- Available in various denominations (0.5 grams to 50 grams)

- BIS hallmarked for purity assurance

- No annual charges

- Instant liquidity

What to Look For:

- BIS hallmark certification (mandatory since June 2021)

- Tamper-proof packaging

- Buy-back policy from seller

- Proper documentation for resale

Price Components:

- Gold price + making charges (typically 5-10% for coins) + GST (3%)

2025 Trend: More than 40 tons of gold was sold in India on the first day of Diwali 2025, with investment products like coins and bars stealing the spotlight from jewelry.

6. Gold Jewelry

Best for: Traditional buyers seeking cultural and personal value

Buying gold jewelry remains the most traditional and sentimental form of investment in India. It holds deep cultural significance, especially during festivals and weddings.

Key Benefits:

- Cultural and emotional value

- Can be worn and enjoyed

- Excellent gifting option

- Accepted everywhere in India

Considerations:

- High making charges (15-25% for intricate designs)

- Lower purity (typically 22 karat)

- Resale value lower due to making charges

- Security concerns

- Styles may become outdated

2025 Market Insight: Jewelry sales dropped by about 30% this festive season compared to last year, as investors shifted toward coins and bars for better returns.

7. Gold Savings Schemes

Best for: Families planning weddings or large purchases

Many jewelers offer gold savings plans where you deposit a fixed sum every month for a chosen duration (typically 11-12 months). At the end of the term, you can buy gold or jewelry worth the accumulated amount, often with an added bonus or discount from the jeweler.

Key Benefits:

- Disciplined saving approach

- Jeweler bonus (typically one month’s installment)

- Flexible monthly amounts

- No documentation hassles

- Fixed making charges

Important Checks:

- Jeweler’s reputation and longevity

- Clear terms and conditions

- Exit policy if you need to withdraw early

- Price lock-in mechanism

- Actual discount versus market rates

Which Gold Investment Option is Best for You?

How to Create a Balanced Gold Investment Plan for 2025

Step 1: Define Your Financial Objectives

Before investing in gold, clarify your financial goals. Are you seeking:

- Security and capital protection?

- Long-term wealth creation?

- Portfolio diversification?

- Hedge against inflation?

Step 2: Determine Optimal Allocation

Financial experts typically suggest allocating 10-15% of your overall portfolio to gold. Financial advisors now recommend clients allocate 5-10% of their portfolio to gold, given the continuing rally.

Step 3: Choose Investment Type Based on Goals

For Short-Term Goals (1-3 years):

- Digital gold for flexibility

- Gold ETFs for liquidity

- Physical gold coins for immediate needs

For Medium-Term Goals (3-5 years):

- Gold mutual funds with SIP

- Combination of ETFs and physical gold

- Gold savings schemes for specific purchases

For Long-Term Goals (5+ years):

- Sovereign Gold Bonds (best tax efficiency)

- Systematic investment in gold mutual funds

- Mix of physical and paper gold

Step 4: Implement Systematic Investment

Setting up a Systematic Investment Plan (SIP) in gold mutual funds helps you invest consistently and benefit from rupee cost averaging during market fluctuations over time.

Sample Gold SIP Strategy:

- ₹5,000/month in gold mutual fund

- ₹3,000/quarter in digital gold

- Annual purchase of 2-5 gram gold coins during festivals

Step 5: Review and Rebalance

Review your gold allocation quarterly. If gold has outperformed and now constitutes 20% of your portfolio instead of the target 15%, consider rebalancing by taking profits.

Current Gold Market Outlook for Festive Season 2025

Strong Festive Demand

Festive demand around Diwali and Dhanteras was reportedly strong despite record-high prices, driven primarily by investment-oriented buying, particularly bars and coins.

Wedding Season Boost Ahead

The busy wedding season over November to March, with a high number of anticipated weddings, is expected to support jewelry demand. This seasonal pattern typically creates upward pressure on gold prices.

Import Surge Indicates Confidence

India’s gold imports surged to a ten-month high in September, totaling $9.16 billion, marking a 77% month-over-month increase. This reflects both seasonal buying ahead of festivals and robust investment demand.

Digital Gold Adoption Growing

Digital gold purchases rose 62% month-over-month to ₹22 billion in October, with volume increasing 45% to 1.8 tonnes, highlighting the growing preference for convenient digital platforms.

Tax Implications on Gold Investments

Understanding tax treatment is crucial for maximizing returns:

Physical Gold (Jewelry, Coins, Bars)

- Short-term capital gains (held less than 36 months): Taxed as per your income tax slab

- Long-term capital gains (held more than 36 months): 20% with indexation benefit

Gold ETFs and Gold Mutual Funds

- Short-term capital gains (held less than 36 months): Taxed as per your income tax slab

- Long-term capital gains (held more than 36 months): 20% with indexation benefit

Sovereign Gold Bonds

- Interest income: Taxed as per your income tax slab

- Capital gains on redemption (at maturity after 8 years): Tax-free

- Capital gains on premature sale (before maturity): Subject to capital gains tax

GST on Gold

- GST Rate: 3% on gold purchases

- Applicable on: Physical gold, digital gold, gold coins

- Not applicable on: Gold ETFs, Gold Mutual Funds (securities transaction)

Smart Tips for Buying Gold This Festive Season

1. Avoid Peak Buying Days

Buy gold 2-3 weeks before the festival when prices are more stable, avoiding Dhanteras day itself when prices are usually higher due to high demand.

2. Compare Prices Across Platforms

Digital gold platforms, banks, jewelers, and online marketplaces may offer different rates. Compare before buying.

3. Check Purity Certifications

Always insist on BIS hallmark certification for physical gold, ensuring 99.5% or 99.9% purity.

4. Understand Making Charges

For jewelry, making charges can range from 8-25%. Negotiate or opt for simpler designs to reduce costs.

5. Keep Documentation Safe

Maintain purchase invoices, certificates, and receipts for resale purposes and tax filing.

6. Consider Buy-Back Policies

Check if your seller offers buy-back facilities, which makes liquidation easier.

7. Monitor Market Trends

Track gold prices for a week before investing to identify favorable entry points.

Common Mistakes to Avoid When Investing in Gold

1. Over-Allocation

Don’t invest more than 15-20% of your portfolio in gold, as it doesn’t generate regular income.

2. Buying at Emotional Peaks

Avoid panic buying during festivals when prices are inflated by demand surges.

3. Ignoring Hidden Costs

Factor in making charges, GST, storage fees, and buy-sell spreads when calculating returns.

4. Choosing Wrong Purity

For investment purposes, stick to 24K or 22K gold. Lower karats have less resale value.

5. Neglecting Diversification

Don’t put all your gold investment in one form—mix physical, digital, and paper gold.

6. Forgetting About Insurance

If holding significant physical gold, consider insurance coverage.

Conclusion: Make Smart Gold Investment Decisions This Festive Season

Investing in gold has always been more than a financial decision in India—it’s a time-honored tradition, especially during festivals like Dhanteras and Diwali. With gold delivering a 67.88% return in 2025, the yellow metal has proven its worth as both a cultural symbol and a solid investment asset.

By choosing reputable platforms, understanding the specifics of your purchase, and exploring modern options such as digital gold, Gold ETFs, and Sovereign Gold Bonds, you can make your investment both safe and rewarding.

Key Takeaways:

- Allocate 10-15% of your portfolio to gold for optimal diversification

- Choose investment type based on your financial goals and time horizon

- Consider systematic investment rather than lump-sum purchases

- Stay informed about market trends and current prices

- Factor in all costs including making charges, GST, and storage fees

- Maintain proper documentation for tax purposes

Gold not only helps preserve wealth but also adds stability and balance to your overall investment portfolio. With the right strategy, it can serve as a hedge against market volatility and inflation while offering long-term growth potential.

Whether you invest in physical gold for tradition or digital instruments for convenience, a well-planned gold investment can be a valuable pillar of your financial future, blending culture, security, and smart wealth management.

Happy Investing This Festive Season!

Disclaimer: Gold prices are subject to market fluctuations. The information provided is for educational purposes only and should not be considered financial advice. Consult with a certified financial advisor before making investment decisions.

Frequently Asked Questions (FAQs)

Q1: What is the best time to buy gold during the festive season? A: Buy 2-3 weeks before major festivals when prices are more stable. Avoid peak days like Dhanteras when demand-driven premiums are highest.

Q2: How much gold should I buy as an investment? A: Financial experts recommend allocating 10-15% of your investment portfolio to gold for optimal diversification.

Q3: Is digital gold safe? A: Yes, digital gold from reputable platforms like Paytm, PhonePe, or Google Pay is safe. The gold is stored securely with trusted partners like SafeGold or MMTC-PAMP.

Q4: Which is better: Gold ETFs or Sovereign Gold Bonds? A: For long-term investment (8+ years), SGBs are better due to 2.5% interest and tax-free capital gains. For liquidity and active trading, Gold ETFs are preferable.

Q5: Do I need to pay GST on gold? A: Yes, 3% GST is applicable on physical gold, digital gold, and gold coins. However, Gold ETFs and mutual funds are exempt as they’re treated as securities.

Q6: Can I convert digital gold to physical gold? A: Yes, most digital gold platforms allow conversion to physical gold (coins/bars) with minimum quantity requirements, typically 0.5 grams or more.

Q7: What is the lock-in period for Sovereign Gold Bonds? A: SGBs have a tenure of 8 years with an exit option from the 5th year onwards. Early redemption is allowed on interest payment dates.

Q8: Are gold returns taxable? A: Yes. Short-term gains (less than 36 months for physical gold) are taxed as per your income slab. Long-term gains attract 20% tax with indexation benefit. SGB gains at maturity are tax-free.